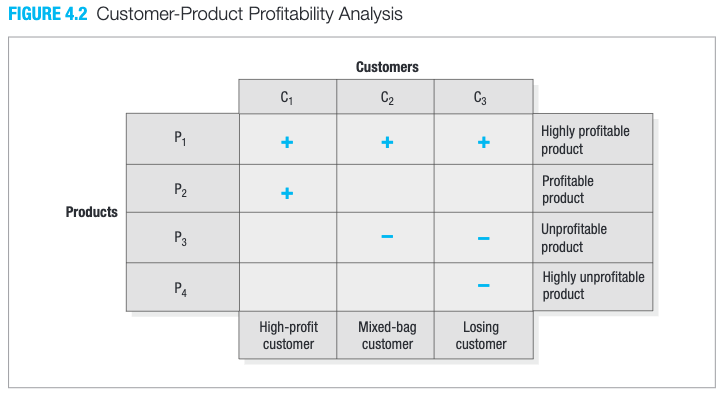

Customer 1 is very profitable; he buys two profit-making products.

Customer 2 yields mixed profitability; she buys one profitable product and one unprofitable product.

Customer 3 is a losing customer because he buys one profitable product and two unprofitable products.

What can the company do about customers 2 and 3?

It can raise the price of its less profitable products or eliminate them, or

it can try to sell customers 2 and 3 its profit-making products. In fact, the company should encourage them to switch to competitors.